Is the latest frenzy like tulipmania, a gold rush or the dotcom boom?

..

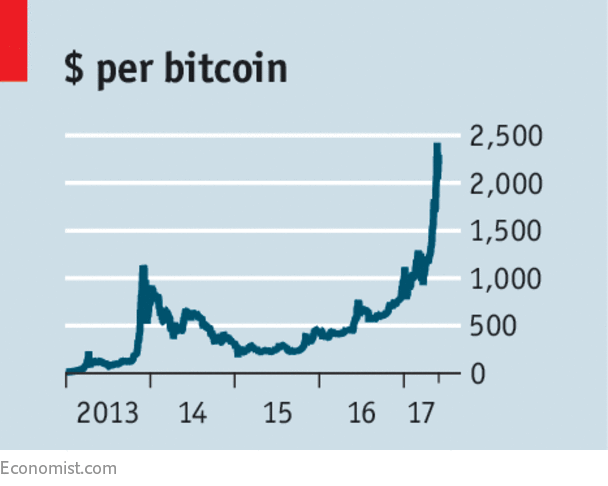

MARKETS frequently froth and bubble, but the boom in bitcoin, a digital currency, is extraordinary. Although its price is down from an all-time high of $2,420 on May 24th, it has more than doubled in just two months. Anyone clever or lucky enough to have bought $1,000 of bitcoins in July 2010, when the price stood at $0.05, would now have a stash worth $46m. Other cryptocurrencies have soared, too, giving them a collective market value of about $80bn. Ascents this steep are rarely sustainable. More often than not, the word “bitcoin” now comes attached to the word “bubble”. But the question of what has driven up the price is important. Is this just a speculative mania, or is it evidence that bitcoin is taking on a more substantial role as a medium of exchange or a store of value? Put another way, is bitcoin like a tulip, gold or the dollar—or is it something else entirely?

Start with the case that this is nothing more than a virtual tulipmania, a speculative hysteria in which a rising price encourages ever more buyers, no matter what the asset is. Bitcoin’s recent trajectory certainly seems manic. Retail investors have piled in. Many already familiar with bitcoin investing have moved on to bet on alternatives, such as Ethereum, and “initial coin offerings” (ICOs), in which firms issue digital tokens of their own.

It looks like a scammers’ paradise, yet unlike tulips, bitcoins have real uses. They now buy everything from pizzas to computers. So if a tulip isn’t the right analogue, how about gold? Bitcoins certainly seem to bear more than a passing resemblance. Goldbugs mistrust governments and their money-printing tendencies; so too do bitcoinesseurs: no central bank is in charge of bitcoin. But a store of value should not bounce around as much as this one does: bitcoin swung from more than $1,100 in late 2013 to less than $200 a year later, before climbing, in fits and starts, to its current dizzying heights.

Rather than being just a form of digital gold, bitcoin aspires to loftier goals: to be a means of exchange like the euro, yen or the dollar. Regulators are starting to take bitcoin seriously. Some of the price surge can be explained by Japan’s decision to treat bitcoin more like any other currency. Yet the bitcoin system is operating at its limits and its developers cannot agree on how to increase the number of exchanges the system is able to handle. As a result, a transaction now costs nearly $4 in fees on average and takes many tedious hours to confirm. For convenience, a dollar bill beats it hands down.

Advertisement:Replay Ad

Advertisement

3

Not so dotty

If bitcoin and the other cryptocurrencies are unlike anything else, what are they? The best comparison may be with the internet and the dotcom boom it created in the late 1990s. Like the internet, cryptocurrencies both embody innovation and give rise to more of it. They are experiments in themselves of how to maintain a public database (the “blockchain”) without anybody in particular, a bank, say, being in charge. Georgia, for instance, is using the technology to secure government records. And blockchains are platforms for further experiments. Take Ethereum, for example. It allows all kinds of projects, from video games to online markets, to raise funds by issuing tokens—essentially private money that can be traded and used within these projects. Although such ICOs need to be handled with care, they could also generate intriguing inventions. Fans hope that they will give rise to decentralised upstarts taking aim at today’s oligopolistic technology giants, such as Amazon and Facebook.

This may seem like a dangerous way to generate innovation. Investors could lose their shirts; a crash in one asset class could spread to others, creating wobbles in the financial system. But in the case of cryptocurrencies such risks seem limited. It is hard to argue that those buying cryptocurrencies are unaware of the risks. And since they are still a fairly self-contained system, contagion is unlikely.

If there is such a thing as a healthy bubble, this is it. To be sure, regulators should watch out that cryptocurrencies do not become even more of a conduit for criminal activity, such as drug dealing. But they should think twice before coming down hard, particularly on ICOs. Being too spiky would not just prick a bubble, but also prevent a lot of the useful innovation that is likely to come about at the same time.

0 comments:

Publicar un comentario