Greece’s Long Debt Journey Tests Europe

Europe has a big challenge to address as Greece’s debt is set to balloon, the IMF says

By Richard Barley

July 15, 2015 11:48 a.m. ET

Greek Finance Minister Euclid Tsakalotos speaks with Christine Lagarde, managing director of the International Monetary Fund, during a meeting of eurozone finance ministers in Brussels on Sunday. Photo: Agence France-Presse/Getty Images

Greek Finance Minister Euclid Tsakalotos speaks with Christine Lagarde, managing director of the International Monetary Fund, during a meeting of eurozone finance ministers in Brussels on Sunday. Photo: Agence France-Presse/Getty Images The scale of the collapse in Greece’s finances in the past year is emerging. It is both an indictment of the Greek government’s actions and a big challenge to Europe. Returning Greece to market financing—the ultimate aim of a bailout package—will be harder the second time around.

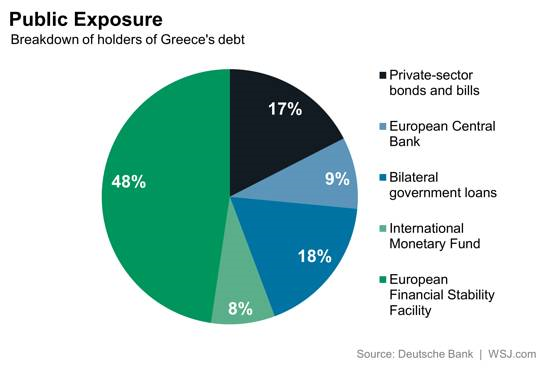

Papers from the International Monetary Fund and the European Commission show how far off track Greece has gone. Last summer, the IMF thought debt might be 105% of gross domestic product by 2022. But three weeks ago, it warned that as a result of the downturn in the Greek economy and the policy choices of the new government, debt would hit 142% of GDP by 2022.

Now, it thinks debt will be 170% of GDP by that date.

There has been a welcome shift away from these headline numbers to take account of the debt relief already provided to Greece by extending maturities and cutting interest rates. A better measure is Greece’s annual gross financing needs as a percentage of GDP. But even this approach shows problems. The IMF thinks this number needs to be below 15% to ensure sustainability. The Commission says that due to the hit to the Greek economy including capital controls and bank closures, financing needs for 2015-2030 rise above 15% “in a number of years.” In the short term, it forecasts two years of recession, with growth only returning in 2017.

The contrast with a year ago, when Greece had regained market access, selling three- and five-year bonds, is enormous. Even at the time there were question marks over whether investors were adequately pricing Greek risk; those bonds are now quoted at 60-70% of face value. By the time Greece tries again, investors may no longer be so engaged in a feverish search for yield; global interest rates may well be higher.

0 comments:

Publicar un comentario