Free exchange

The opposite of insurance

A new book argues that household debt, not broken banks, fuelled the recent recession

May 17th 2014

BEFORE Ben Bernanke found himself trying to prevent a second Great Depression as chairman of the Federal Reserve, he had become well known in economic circles for explaining why the first one happened. In a paper published in 1983, Mr Bernanke blamed the collapse of the banking system for constricting the supply of credit, which “helped convert the severe but not unprecedented downturn of 1929-30 into a protracted depression”.

The notion that financial crises are transmitted to the broader economy by the “bank-lending channel” has dominated subsequent policymaking. It is why Mr Bernanke fought so hard to stop the panic in 2008 and to recapitalise the banking system afterwards. Tim Geithner, who was at the Fed with Mr Bernanke and then became Barack Obama’s treasury secretary, spends much of his new memoir reiterating their argument: “When the financial system stops working, credit freezes, savings evaporate and demand for goods and services disappears, which leads to lay-offs and poverty and pain.”

Another new book*, by Atif Mian of Princeton University and Amir Sufi of the University of Chicago, challenges this orthodoxy. The real cause of the post-crisis slump, they argue, was not the damage to the banks, but the run-up in household debt that came before, which became an anchor on consumption when home prices subsequently collapsed. Shifting focus from banks to households, in turn, leads them to very different remedies, the most radical of which is to replace many loans with equity-like contracts in which lenders share losses with borrowers.

By analysing the relationship between consumption, employment, home equity and other debts and assets by county, Messrs Mian and Sufi find that consumption fell most sharply in counties that experienced the biggest drop in residents’ net worth. This, they argue, would not be the case if the primary restraint on consumption was damage to the banks brought on by the collapse of Lehman Brothers. They found similar evidence in county-level employment. In counties where net worth fell most, jobs were slashed not by small companies, which depend most on banks, but big ones—because sales were slumping.

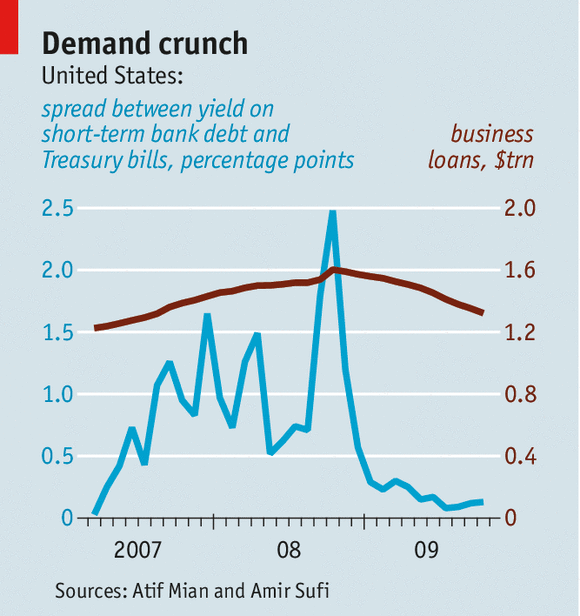

Moreover, banks’ difficulties, as measured by the spread between yields on their short-term debt and that of the government, peaked in late 2008. Yet banks’ lending to business was actually expanding at the time. By the end of the year the spread had returned to normal thanks to the Fed’s vigorous intervention, but bank lending began to contract (see chart).

Messrs Mian and Sufi think bank lending has an unseemly hold on contemporary thought. They fault the Fed and the Treasury for lavishing money on banks to boost the supply of credit when the problem was demand. Poor households’ wealth had evaporated, and with it their desire to borrow, which would have been better dealt with by writing down their mortgages.

There are some flaws to this argument. Falling house prices and net worth help explain why employment started sinking in early 2008, but not why it went into free fall after the failure of Lehman Brothers. By examining only loans from banks to business, they ignore the contraction in consumer credit and in lending by other financial institutions. And had more banks been allowed to fail, the supply of credit would undoubtedly have shrunk further.

The kiss of debt

What is needed, they argue, is to make debt contracts more flexible, and where possible, replace them with equity. Courts should be able to write down the principal of mortgages as an alternative to foreclosure. They recommend “shared-responsibility mortgages” whose principal would decline along with local house prices. To compensate for the risk of loss, lenders, they reckon, would have to charge a fee equal to 1.4% of the mortgage, or receive 5% of any increase in the value of the property.

University education is also ripe for more equity-like financing, since students do not know how much they will eventually earn. In Australia and Britain, they pay a fixed percentage of their income; the authors recommend instead linking repayment to the health of the job market, an idea first proposed by Milton Friedman. They also endorse a proposal by Mark Kamstra and Robert Shiller to link interest on sovereign bonds to gross domestic product. Such an arrangement would have made it easier for the governments of Spain, Greece and Ireland to keep servicing their debts when their economies imploded.

There are many practical obstacles to these ideas. Taxes and regulation, for instance, are biased towards debt; regulators might judge shared-responsibility mortgages too risky for banks.

That hints at a bigger obstacle: while debt may be dangerous for the borrower, it is the opposite for the lender. Savers prefer the safety and predictability of a debt contract, which is why they accept lower returns on bonds over time than on equities. Many debt contracts exist primarily to satisfy this desire for safe assets—most notably bank deposits.

Borrowers, too, may prefer debt, because it allows them to capture the upside of their investment. Most of the time, that optimism is justified. Unfortunately, every generation or so, it ends in calamity.

* “House of Debt: How They (and You) caused the Great Recession, and How We Can Prevent It from Happening Again”, by A. Mian and A. Sufi. University of Chicago Press.

0 comments:

Publicar un comentario