Demography, growth and inequality

Age invaders

A generation of old people is about to change the global economy. They will not all do so in the same way

Apr 26th 2014

.

IN THE 20th century the planet’s population doubled twice. It will not double even once in the current century, because birth rates in much of the world have declined steeply. But the number of people over 65 is set to double within just 25 years. This shift in the structure of the population is not as momentous as the expansion that came before. But it is more than enough to reshape the world economy.

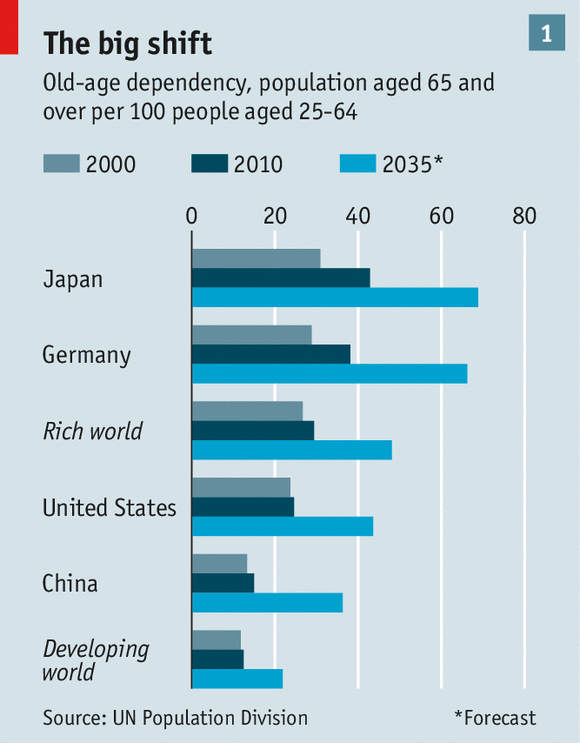

According to the UN’s population projections, the standard source for demographic estimates, there are around 600m people aged 65 or older alive today. That is in itself remarkable; the author Fred Pearce claims it is possible that half of all the humans who have ever been over 65 are alive today. But as a share of the total population, at 8%, it is not that different to what it was a few decades ago.

By 2035, however, more than 1.1 billion people—13% of the population—will be above the age of 65. This is a natural corollary of the dropping birth rates that are slowing overall population growth; they mean there are proportionally fewer young people around. The “old-age dependency ratio”—the ratio of old people to those of working age—will grow even faster. In 2010 the world had 16 people aged 65 and over for every 100 adults between the ages of 25 and 64, almost the same ratio it had in 1980. By 2035 the UN expects that number to have risen to 26.

In rich countries it will be much higher (see chart 1). Japan will have 69 old people for every 100 of working age by 2035 (up from 43 in 2010), Germany 66 (from 38).

Even America, which has a relatively high fertility rate, will see its old-age dependency rate rise by more than 70%, to 44. Developing countries, where today’s ratio is much lower, will not see absolute levels rise that high; but the proportional growth will be higher. Over the same time period the old-age dependency rate in China will more than double from 15 to 36. Latin America will see a shift from 14 to 27.

Three ways forward

The received wisdom is that a larger proportion of old people means slower growth and, because the old need to draw down their wealth to live, less saving; that leads to higher interest rates and falling asset prices. Some economists are more sanguine, arguing that people will adapt and work longer, rendering moot measures of dependency which assume no one works after the age of 65. A third group harks back to the work of Alvin Hansen, known as the “American Keynes”, who argued in 1938 that a shrinking population in America would bring with it diminished incentives for companies to invest—a smaller workforce needs less investment—and hence persistent stagnation.

The unexpected baby boom of 1946-64 messed up Hansen’s predictions, and unforeseen events could undermine today’s demographic projections, too—though bearing in mind that the baby boom required a world war to set the stage, that should not be seen as a source of hope. But if older people work longer and thus save longer, while slowing population growth means firms have less incentive to invest, something close to what Hansen envisaged could come about even without the sort of overall population decline he foresaw.

A few months ago Larry Summers, a Harvard professor and former treasury secretary, argued that America’s economy appeared already to be suffering this sort of “secular stagnation”—a phrase taken directly from Hansen.

Who is right? The answer depends on examining the three main channels through which demography influences the economy: changes in the size of the workforce; changes in the rate of productivity growth; and changes in the pattern of savings. The result of such examination is not conclusive. But, for the next few years at least, Hansen’s worries seem most relevant, not least because of a previously unexpected effect: the tendency of those with higher skills to work for longer, and more productively, than they have done to date.

The first obvious implication of a population that is getting a lot older without growing much is that, unless the retirement age changes, there will be fewer workers. That means less output, unless productivity rises to compensate. Under the UN’s standard assumption that a working life ends at 65, and with no increases in productivity, ageing populations could cut growth rates in parts of the rich world by between one-third and one-half over the coming years.

Have skills, will work

The real size of the workforce, though, depends on more than the age structure of the population; it depends on who else works (women who currently do not, perhaps, or immigrants) and how long people work. In the late 20th century that last factor changed little. An analysis of 43 mostly rich countries by David Bloom, David Canning and Günther Fink, all of Harvard University, found that between 1965 and 2005 the average legal retirement age rose by less than six months. During that time male life expectancy rose by nine years.

Since the turn of the century that trend has reversed. Almost 20% of Americans aged over 65 are now in the labour force, compared with 13% in 2000. Nearly half of all Germans in their early 60s are employed today, compared with a quarter a decade ago.

This is in part due to policy. Debt-laden governments in Europe have cut back their pension promises and raised the retirement age. Half a dozen European countries, including Italy, Spain and the Netherlands, have linked the statutory retirement age to life expectancy. Personal financial circumstances have played a part, too. In most countries the shift was strongest in the wake of the 2008 financial crisis, which hit the savings of many near-retirees. The move away from corporate pension plans that provided a fraction of the recipient’s final salary in perpetuity will also have kept some people working longer.

But an even more important factor is education. Better-educated older people are far more likely to work for longer. Gary Burtless of the Brookings Institution has calculated that, in America, only 32% of male high-school graduates with no further formal education are in the workforce between the ages of 62 and 74. For men with a professional degree the figure is 65% (though the overall number of such men is obviously smaller).

For women the ratios are one-quarter versus one-half, with the share of highly educated women working into their 60s soaring (see chart 2). In Europe, where workers of all sorts are soldiering on into their 60s more than they used to, the effect is not quite as marked, but still striking. Only a quarter of the least-educated Europeans aged 60-64 still work; half of those with a degree do.

It is not a hard pattern to explain. Less-skilled workers often have manual jobs that get harder as you get older. The relative pay of the less-skilled has fallen, making retirement on a public pension more attractive; for the unemployed, who are also likely to be less skilled, retirement is a terrific option. Research by Clemens Hetschko, Andreas Knabe and Ronnie Schöb shows that people who go straight from unemployment to retirement experience a startling increase in their sense of well-being.

Higher-skilled workers, on the other hand, tend to be paid more, which gives them an incentive to keep working. They are also on average healthier and longer-lived, so they can work and earn past 65 and still expect to enjoy the fruits of that extra labour later on.

This does not mean the workforce will grow. Overall work rates among the over-60s will still be lower than they were for the same cohort when it was younger. And even as more educated old folk are working, fewer less-skilled young people are. In Europe, jobless rates are highest among the least-educated young. In America, where the labour participation rate (at 63%) is close to a three-decade low, employment has dropped most sharply for less-skilled men. With no surge in employment among women, and little appetite for mass immigration, in most of the rich world the workforce looks likely to shrink even if skilled oldies stay employed.

Legacy of the void

And ageing societies may ossify. Alfred Sauvy, the French thinker who coined the term “third world”, was prone to worry that the first world would become “a society of old people, living in old houses, ruminating about old ideas”. Japan’s productivity growth slowed sharply in the 1990s when its working-age population began to shrink; Germany’s productivity performance has become lacklustre as its population ages.

But Japan’s slowed productivity growth can also be ascribed to its burst asset bubble, and Germany’s to reforms meant to reduce unemployment; both countries, ageing as they are, score better in the World Economic Forum’s ranking for innovation than America. A dearth of workers might prompt the invention of labour-saving capital-intensive technology, just as Japanese firms are pioneering the use of robots to look after old people. And a wealth of job experience can counter slower cognitive speed. In an age of ever-smarter machines, the attributes that enhance productivity may have less to do with pure cognitive oomph than motivation, people skills and managerial experience.

Perhaps most important, better education leads to higher productivity at any age. For all these reasons, a growing group of highly educated older folk could increase productivity, offsetting much of the effect of a smaller workforce.

Evidence on both sides of the Atlantic bears this out. A clutch of recent studies suggests that older workers are disproportionately more productive—as you would expect if they are disproportionately better educated. Laura Romeu Gordo of the German Centre of Gerontology and Vegard Skirbekk, of the International Institute for Applied Systems Analysis in Austria, have shown that in Germany older workers who stayed in the labour force have tended to move into jobs which demanded more cognitive skill. Perhaps because of such effects, the earnings of those over 50 have risen relative to younger workers.

Saving graces

This could be good news for countries with well-educated people currently entering old age—but less so in places that are less developed. Nearly half of China’s workers aged between 50 and 64 have not completed primary school. As these unskilled people age, their productivity is likely to fall. Working with his IIASA colleagues Elke Loichinger and Daniela Weber, Mr Skirbekk tried to gauge this effect by creating a “cognition-adjusted dependency ratio”. They compared the cognitive ability of people aged 50 and over across rich and emerging economies by means of an experiment which tested their ability to recall words, and used the results to weight dependency ratios. This cognition-adjusted ratio is lower in northern Europe than it is in China, even though the age-based ratio is far higher in Europe, because the elderly in Europe score much more strongly on the cognitive-skill test. Similarly adjusted, America’s dependency ratio is better than India’s.

If skill and education determine how long and how well older people work, they also have big implications for saving, the third channel through which ageing affects growth. A larger group of well-educated older people will earn a larger share of overall income. In America the share of male earnings going to those aged 60-74 has risen from 7.3% to 12.7% since 2000 as well-educated baby-boomers have moved into their 60s.

Some of these earnings will finance retirement, when those concerned finally decide to take it; more savings by people in their 60s will be matched by more spending when they reach their 80s. But many of the educated elderly are likely to accumulate far more than they will draw down towards the end of life.

Circumstantial evidence supports this argument. Thomas Piketty, a French economist, calculates that the average wealth of French 80-year-olds is 134% that of 50- to 59-year-olds, the highest gap since the 1930s. For the next few years at least, skill-skewed ageing is likely to mean both more inequality and more private saving.

At the same time governments across the rich world (and particularly in Europe) are trimming their pension promises and cutting their budget deficits, both of which add to national saving. Reforms designed to trim future pensions mean that, regardless of their skill level, those close to retirement are likely to save more and that governments will spend less per old person. The European Commission’s latest forecasts suggest overall pension spending in the EU will fall by 0.1% of GDP between 2010 and 2020, before rising by 0.6% in the subsequent decade. That is not insignificant, but it is far less than some of the breathless commentary about the “burden” of ageing implies.

Taken together, the net effect of high saving by educated older workers and less-generous pensions is likely to be an unexpected degree of thrift in the rich world, at least for the next few years. If the money saved finds productive investment opportunities it has the potential to boost long-run growth. But where will these opportunities be? In principle, two possibilities stand out. One is rapid innovation in advanced economies. The second is fast growth in emerging economies—especially younger, poorer ones.

Unfortunately, more capital currently flows out of emerging economies into the rich world than the other way. The most successful emerging economies have built up huge stashes of foreign currency; many are leery of depending too much on foreign borrowing. Even if that were to change, the youthful economies of south Asia and Africa are too small to absorb huge flows of capital from those countries that are ageing fast.

And in the rich world, despite lots of obvious innovation, particularly in computer technology, both productivity growth and investment have been tepid of late. That may be a hangover from the financial crisis. But it could also be a structural change. The price of capital goods, notably anything to do with computers, has fallen sharply; it may be that today’s innovation is simply less investment-intensive than it was in the manufacturing age. And the ageing population itself may deter investment. Fewer workers, other things being equal, means the economy needs a smaller capital stock, even if some of those workers are clever old sticks.

And an ageing population spends differently. Old people buy fewer things that require heavy investment—notably houses—and more services, whether in health care or tourism.

Not destiny, but not nothing

On both sides of the Atlantic, recent budget decisions appear to reflect the priorities of the ageing and affluent. Annuities reform in Britain increased people’s freedom to spend their pension pots; the disappearance of property-tax reform spared homeowning older Italians a new burden; America’s budget slashed spending on the young and poor while failing to make government health and pension spending any less generous to the well-off. Few rich-country governments have shown any appetite for large-scale investment, despite low interest rates.

A set of forces pushing investment down and pushing saving up, with no countervailing policy response, makes the impact of ageing over the next few years look like the world that Hansen described: one of slower growth (albeit not as slow as it would have been if older folk were not working more), a surfeit of saving and very low interest rates. It will be a world in which ageing reinforces the changes in income distribution that new technology has brought with it: the skilled old earn more, the less-skilled of all ages are squeezed. The less-educated and jobless young will be particularly poorly served, never building up the skills to enable them to become productive older workers.

Compared with the dire warnings about the bankrupting consequences of a “grey tsunami”, this is good news. But not as good as all that.

0 comments:

Publicar un comentario